A Definitive Guide for Ugandan Businesses on Transactions with Non-Resident Associates

- Business

- 2025-07-31

- 05 Comments

An Expert Report from Continental Tax Trade

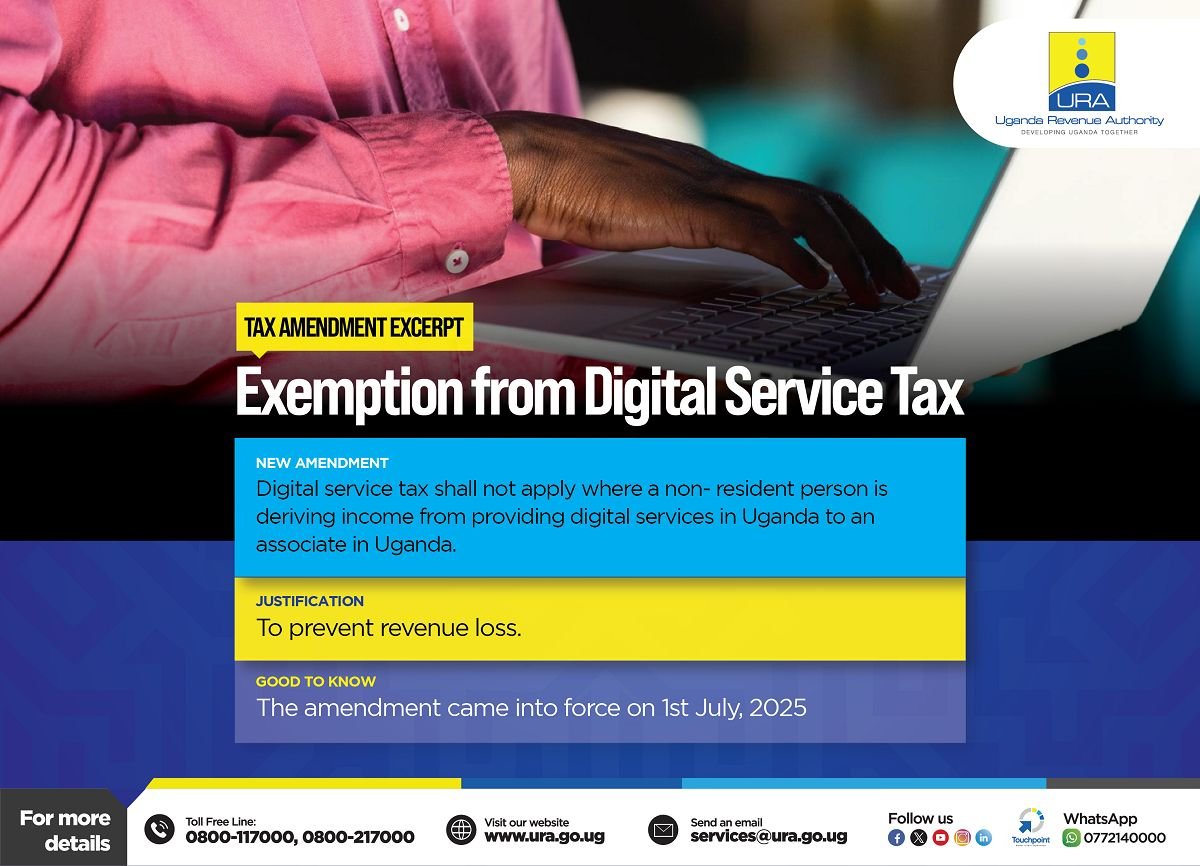

Effective 1st July 2025, the Government of Uganda has significantly altered the taxation of digital services provided by non-resident companies to their related entities in Uganda. Through the Income Tax (Amendment) Act, 2025, these specific transactions are now exempt from the 5% Digital Services Tax (DST).

A critical implication of this new policy is the transfer of the tax compliance obligation. Previously, under the DST regime introduced in 2023, the non-resident service provider was responsible for registering with the Uganda Revenue Authority (URA), filing returns, and remitting the 5% tax on their gross Ugandan-sourced revenue.

Continental Tax Trade strongly advises all clients to undertake an immediate and thorough review of their service agreements with all non-resident digital providers to determine if an "associate" relationship exists under Ugandan law. This assessment is crucial to identify transactions now liable for the 15% WHT and to avoid significant penalties for non-compliance. Businesses must update their payment and accounting systems to ensure the correct deduction and timely remittance of the WHT to the URA. Furthermore, we recommend a comprehensive review of inter-company service agreements and transfer pricing documentation to ensure they can withstand the heightened scrutiny from the URA on related-party transactions that this new legislation inevitably brings.